Coverage of Water Damage

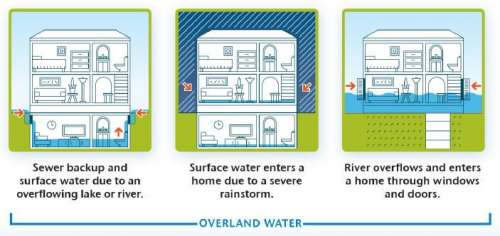

On the beginning, there is one kind of water damage in the insurance policy. It is a sewer backup. Now there is two more new coverage about water. Here is a sample from Optimumwest insurance company. Sewer Backup Water...

Tech geek. Life geek.

On the beginning, there is one kind of water damage in the insurance policy. It is a sewer backup. Now there is two more new coverage about water. Here is a sample from Optimumwest insurance company. Sewer Backup Water...

The insurance industry and government have a long tradition of working together in a social contract to provide relatively seamless compensation to citizens who suffer devastating losses of property. The insurance industry takes most of the risks (e.g., fire, theft,...

In Canada, an overlooked class of insurance is legal expenses insurance (or legal protection insurance in some countries), which can provide coverage for legal costs associated with disputes and issues not covered by the typical and common commercial policies. Legal...

Shallow 5.1 earthquake rattles Los Angeles. More than 100 aftershocks follow Friday night quake. vi CBC Experts suggest there is 30% chance of a significant damaging earthquake concurrence in British Columbia with in the next fifty years. An earthquake like...

First of all, the building is covered by your Strata insurance policy. So, no need to worry too much about your building, including structure, roof, wall, etc. But the others are not covered by your strata insurance policy. That is...